Estimating die casting costs is crucial for engineers and purchasing teams to ensure predictable budgets and competitive pricing.

While die casting offers high precision and excellent surface finish, its costs are influenced by factors like tooling, materials, production, machining, and inspection.

The Main Components of Die Casting Cost

Die casting costs can be categorized into several major components:

- Tooling and Die Cost

- Material Cost

- Production (Pressing) Cost

- Labor and Overhead

- Secondary Machining and Finishing Cost

- Inspection and Quality Assurance

- Scrap, Rework, and Yield Loss

Each category has its own drivers and considerations, and together they form the basis of a comprehensive cost model.

1. Tooling and Die Cost

Tooling cost is typically the highest upfront cost in a die casting project. It covers the design, engineering, machining, heat treating, and assembly of the die, the steel mold that shapes the molten metal. Dies can be simple (single cavity) or complex (multi-cavity with slides, cores, and cooling channels), and their design affects virtually all downstream cost factors.

What Influences Tooling Cost

Part Geometry Complexity

- Complex parts require more intricate tooling with slides, lifters, and inserts.

- Undercuts and thin walls increase machining time and tooling precision requirements.

Cavity Count

Multi-cavity dies produce more parts per cycle, reducing per-part tooling costs in high volumes, but they are more expensive to manufacture.

Tolerance and Surface Finish Requirements

Precision machining and further polishing are necessary for precise surface finishes and tight tolerances.

Die Material and Expected Life

High-performance tool steels and coatings extend die life but increase initial cost.

Typical Tooling Cost Ranges

| Die Type | Typical Cost Range | Notes |

| Simple, single cavity | $5,000–$15,000 | Basic parts |

| Moderate complexity | $15,000–$40,000 | Detailed geometry |

| Complex with slides/inserts | $40,000 – $100,000+ | Multi-feature parts |

| High-volume multi-cavity | $100,000+ | Very large programs |

The die cost must be amortized over the expected production volume to calculate its contribution to the per-part cost.

Tooling Amortisation Example

If a die costs $50,000 and is expected to produce 200,000 parts:

Tooling cost per part=$50,000/200,000=$0.25

This figure becomes a baseline in your per-part cost estimate.

2. Material Cost

Material cost is the expense of the metal used in casting each part. It is a function of part weight, alloy price, and material yield (metal lost as scrap or unusable flash).

How to Calculate Material Cost

Material cost per part = Part weight (kg) × Alloy price per kg

Typical alloy prices (approximate and variable with market conditions):

- Aluminium alloys: $2.50 – $4.00/kg

- Zinc alloys: $2.00 – $3.50/kg

- Magnesium alloys: $3.50 – $6.00+/kg

- Copper alloys: $5.00 – $10.00+/kg

Scrap and Yield Considerations

Die casting naturally produces excess metal as runners, gates, and flash. If the supplier can reclaim and remelt this material, the effective material cost decreases. Discuss yield and recycling capabilities with foundries when estimating material costs.

3. Production (Pressing) Cost

Production cost captures the variable cost of running the die casting machine, essentially the energy, maintenance, and machine depreciation associated with each cycle.

How to Estimate Pressing Cost

Production cost per part = Hourly machine cost/Parts produced per hour

Example:

If a press costs $60/hour and produces 800 parts per hour:

Production cost per part = $60/800 = $0.075

This is a baseline estimate. Add auxiliary costs for gas, cooling, and machine setup time as needed.

4. Labor and Overhead

Labor costs cover the work of operators, setup personnel, and material handlers, while overhead refers to indirect expenses such as supervision, facility utilities, insurance, and administrative services.

Estimating Labor Cost

Estimate total labor hours needed for setup, cast run, monitoring, and packaging, and multiply by an appropriate labor rate.

Example:

If total labor hours for a run are 30 hours at $30/hour across a production of 100,000 parts:

30×$30=$900

Labor cost per part=$900/100,000=$0.009

Overhead is typically applied as a percentage of labor or machine cost and must be allocated accordingly.

5. Secondary Machining and Finishing

Many die-cast parts require secondary operations to achieve critical dimensions or surface properties, including CNC machining, tapping, polishing, tumbling, coating, plating, or anodizing.

Typical Secondary Operation Costs

| Operation | Typical Cost/Part |

| Basic machining | $0.50–$2.00 |

| Deburring | $0.10–$0.30 |

| Shot blasting | $0.10–$0.30 |

| Anodizing | $0.40–$1.50 |

| Powder coating | $0.50–$2.00 |

These costs vary widely based on complexity, surface area, and batch size.

6. Inspection and Quality Assurance

Die casting parts often require inspection to verify dimensional accuracy and geometric tolerance. The cost of inspection depends on part complexity and tolerance requirements.

Common Inspection Methods

- Go/No Go gauges

- Coordinate Measuring Machine (CMM)

- Optical inspection

- Non-destructive testing (NDT)

- Statistical Process Control (SPC)

Inspection can be a small incremental cost or a larger investment when high precision or automated systems are involved.

7. Scrap, Rework, and Yield Loss

No manufacturing process is perfect. A percentage of parts will fail inspection or emerge with defects requiring rework or scrap. Include a reasonable contingency in your estimates:

Adjusted cost per good part = Total cost / (1 − Scrap rate)

Example:

If total cost per part is estimated at $2.00 and expected scrap is 3%:

Adjusted cost=2.00/0.97≈$2.06

Factoring scrap ensures your cost model is realistic.

Step-by-Step Die Casting Cost Estimation

Below is a structured process for estimating die casting costs that you can replicate for custom projects:

Step 1: Define Project Requirements

Identify key parameters:

- Material and alloy type

- Target annual/lot volume

- Tolerance and finish requirements

- Secondary operations needed

- Delivery timeline

This sets the foundation for estimating tooling, materials, and process costs.

Step 2: Estimate Tooling Cost

- Analyze part complexity and determine die features.

- Consult with tooling engineers or suppliers for rough die cost.

- Decide cavity count based on projected volume.

Amortize the die cost over expected volume to arrive at per-part tooling contribution.

Step 3: Estimate Material Cost

- Determine part net weight (from CAD/BOM).

- Multiply by alloy price per kg.

- Adjust for material yield based on expected reclaim/recycle rates.

This gives a baseline raw material cost per part.

Step 4: Estimate Production Cost

Use cycle time data (from similar parts or supplier quotes).

Calculate the press hourly cost divided by parts per hour.

Include energy, auxiliary machine usage, and run-up time.

Step 5: Add Labor and Overhead

- Estimate setup, operation, and packaging labor hours.

- Apply appropriate labor rates.

Include a proportional allocation of facility overhead.

Step 6: Add Secondary Machining/Finishing

Based on engineering requirements, add costs for CNC, coating, deburring, polishing, etc.

Get average times and rates either from your shop floor or supplier quotes.

Step 7: Inspection and Quality Cost

- Include fixture or gauge costs amortized over the run if applicable.

Add per-part inspection labor or automated system costs.

Step 8: Adjust for Scrap/Rework and Yield

- Estimate typical defect rate based on historical data or supplier input.

- Adjust the per-good-part cost accordingly.

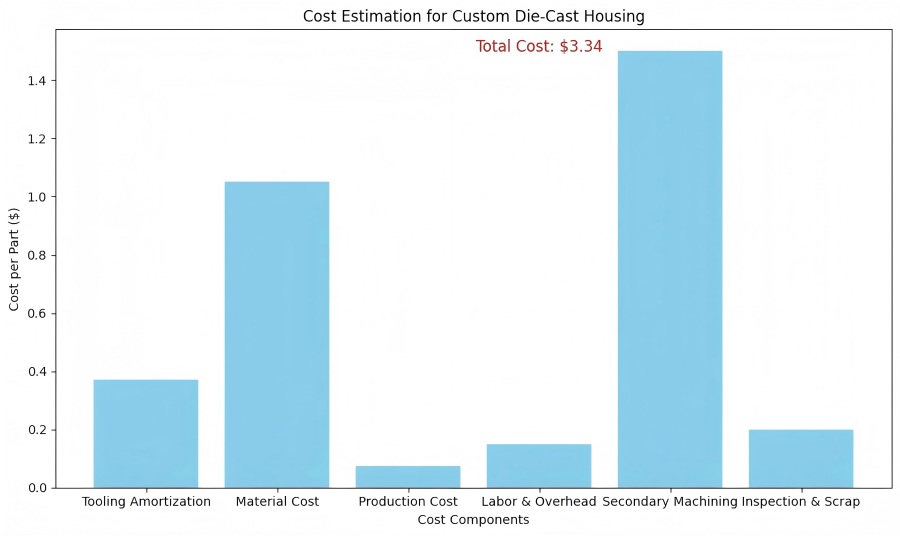

Example: Cost Estimation for Custom Die-Cast Housing

Below is a practical example that applies the above steps to a custom part estimated for an initial production of 150,000 units.

- Part: Die-cast aluminum housing

- Weight: 0.35 kg

- Alloy: Aluminum, $3.00/kg

- Die cost: $55,000

- Press cost: $60/hour

- Production rate: 800 parts/hour

- Labor & overhead: $0.15/part

- Secondary machining: $1.50/part

- Inspection & scrap reserve: $0.20/part

Calculate:

- Tooling Amortization: $55,000÷150,000=$0.37

- Material Cost: 0.35×3.00=$1.05

- Production Cost: $60÷800=$0.075

- Labor & Overhead: $0.15

- Secondary Machining: $1.50

- Inspection & Scrap: $0.20

Total Estimated Cost: 0.37+1.05+0.075+0.15+1.50+0.20≈$3.35 per part

This example illustrates how tooling, material, and machining dominate cost while production and inspection contribute smaller, but still important, amounts.